Quantum Information, Game Theory, and the Future of Rationality

The Market Is a Game—But Which One

We often define market cycles with data-driven labels like "bull" and "bear." But what if those labels are the result of a deeper, hidden strategic game? This post introduces a novel application of inverse game theory to go beyond simple market narratives. By analyzing daily returns, we can reverse-engineer the underlying strategic structure of the market, revealing if it's acting like a Prisoner's Dilemma, Chicken, or another classic game. This approach offers a powerful new lens for understanding market dynamics and a crucial first step toward leveraging quantum strategies in the future.

Faisal Shah Khan, PhD

8/2/20254 min read

I have been working for some time on how markets may unlock new value once networked quantum computers become available—or better yet, once a quantum network arrives, enabling the real-time use of quantum resources like entanglement. The foundation of this idea is a quantum game-theoretic model for trading: a Prisoner’s Dilemma played across a network of quantum computers, using "go long" vs. "go short" as strategies, where the quantum data generated serves as public signals. I have written about this on this blog (Beyond Classical Mediation, Quantum Strategies and Quantum Advantage). A peer-reviewed version of this work was recently published in Quantum Economics and Science.

While that research continues in the quantum direction, it has also drawn attention to a more immediate and foundational question: how do we currently use game theory to understand market behavior? Because the new value promised by quantum Prisoner’s Dilemma trading depends on a critical prerequisite—that traders recognize the game the market is playing. Without this awareness of what I call the market game state, the added value from quantum strategies will remain inaccessible. This raises a practical question: how do traders currently assess this game state? Do they, in practice, try to understand markets in these terms?

Are Traders Already Thinking in Game-Theoretic Terms?

At this year’s Quantum Information Processing (QIP) conference in Raleigh, North Carolina, I presented the quantum Prisoner's Dilemma work as a poster. One especially insightful conversation during the poster session was with a practicing trader. I asked him: Do traders encounter situations that resemble the Prisoner's Dilemma? Specifically, do they recognize market environments where shorting becomes the dominant strategy, even if going long would lead to better overall outcomes?

His answer was essentially yes, but informally. Traders often detect patterns that resemble strategic dilemmas, yet they rarely frame them in formal game-theoretic terms. Instead, they tend to rely on behavioral categories—such as "bulls," "bears," or "momentum chasers"—or psychological archetypes like “greedy versus fearful.” But these are forward-imposed narratives, not strategic structures inferred from data. If we aim to align market behavior with game-theoretic reasoning—and eventually introduce quantum advantages—then we need a method for extracting structure from observation. That method is inverse game theory.

From Observation to Structure: Inverse Game Theory

Inverse game theory reverses the traditional approach. Instead of starting with known payoffs and solving for optimal strategies, we begin with observed outcomes—what actually happened in the market—and attempt to reconstruct the underlying payoff structures that could have produced them. To make this idea concrete, let us consider a basic trading framework: agents can either buy or sell. In securities markets, this takes more specific forms:

Long: Buy and hold, expecting the price to rise.

Short: Sell borrowed shares, expecting the price to fall.

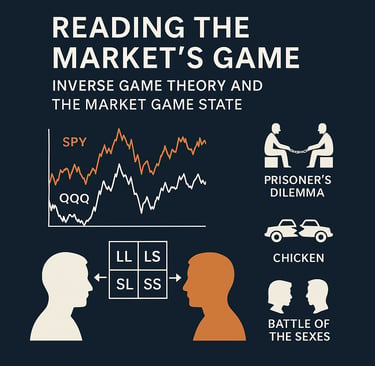

Now consider modeling two large assets—such as SPY (which tracks the S&P 500) and QQQ (which tracks the Nasdaq-100)—as players in a repeated game. We can classify daily price behavior into four combinations:

(long, long) – Both SPY and QQQ had positive returns.

(long, short) – SPY went up, QQQ went down.

(short, long) – SPY went down, QQQ went up.

(short, short) – Both had negative returns.

This forms a 2×2 matrix of strategy combinations, just like in classical game theory. Over time, the frequency of these outcomes reflects an underlying strategic structure. The question becomes: can we detect which structure best describes it?

The Market Game State Model

An implementation of this inverse game-theoretic method for analyzing market behavior can be found at github.com/FShahKhan/market-game-state. The following outlines how the system operates.

Step 1: Classifying Market Behavior

The model retrieves daily return data for SPY and QQQ using the yfinance library.

It classifies each trading day into one of the four strategy combinations: (long,long), (long,short), (short,long), (short,short)

Step 2: Inferring Payoffs from Data

Rather than guessing or assuming payoffs, the model attempts to infer them from the data.

It minimizes KL divergence—a statistical measure of how one probability distribution diverges from another—to compare:

The actual frequency of strategy pairs observed in the market, and

The frequency expected from a candidate payoff structure (Prisoner's Dilemma, for example).

By adjusting the payoffs until these distributions align, the model estimates what reward structure would produce the observed behavior.

Step 3: Realistic Decision-Making with QRE

Markets are noisy and unpredictable. Traders do not always act with perfect rationality.

To account for this, the model applies Quantal Response Equilibrium (QRE), which allows for probabilistic strategy choices.

In QRE, players are more likely to choose higher-payoff strategies, but less favorable options are still chosen with some probability. This models bounded rationality more accurately than traditional equilibrium assumptions.

Step 4: Matching to Known Games

With the inferred payoff rankings for each player, the model compares the structure to standard 2×2 games:

Prisoner’s Dilemma

Chicken

Battle of the Sexes

The model outputs:

The best-matching game type

The payoff rankings for both players

A softmax-based probability score for each game type, reflecting match strength

Why This Matters

This method offers a data-driven way to interpret the market as a strategic system. It does not rely on speculative assumptions about trader psychology. Instead, it asks a simple but powerful question: Given what we observe, what game is being played?

If the market resembles a Prisoner’s Dilemma, traders may be harming each other through individualistic rational behavior (such as aggressive shorting), at the price of reaching socially optimal equilibrium.

If the game resembles Chicken, the market could be in a fragile standoff.

If it matches Battle of the Sexes, then coordination exists but with conflicting priorities.

For classical traders, this insight provides a new tool to interpret price action, sentiment, and risk. For those preparing to leverage quantum strategies, it is indispensable. Quantum strategies depend on game structure—and only outperform under specific strategic conditions.

We often say “the market is a game,” but rarely do we ask which game. The market game state approach helps us answer that question in a rigorous, data-first way. It is a bridge between behavioral storytelling and quantitative structure—and, eventually, a stepping stone to quantum trading.